The Minsky Moment and Theory of Reflexivity: What Minsky and Soros Taught Us About Instability

*Repost from SpeculatorsAnonymous.com

I’ve long believed that markets and economies trend towards disequilibrium (aka a loss of stability). And this is contrary to what we learned in economics – that a system tends towards equilibrium.

And while equilibrium may sound good in theory; it doesn’t hold up in reality.

Why?

Because markets and the economy are complex and dynamic social systems. Meaning they constantly change over time and have ripple effects.

There are eight billion people in the world – both rational and irrational– driven by their own biases. Thus influencing everything around them.

Now, while many may cling to the idea of equilibrium and ‘rational’ markets, there were a few who disagreed with this train of thought and have made compelling findings to the contrary.

But none more so than these two:

Hyman Minsky and his Financial Instability Hypothesis (aka the ‘Minsky Moment’).

And George Soros with his Theory of Reflexivity (aka reflexive financial systems).

Let me explain why they’re so important. . .

Beware the Minsky Moment: How Hyman Minsky and his Financial Instability Hypothesis Work

Hyman Minsky was a post-Keynesian economist that did most of his work in the mid-to-late 1900s. But more than that, he was a brilliant thinker and wrote the groundbreaking book ‘Stabilizing and Unstable Economy’ (1986) – a book I highly recommend reading.

Now, unfortunately, most of Minsky’s work was ignored by mainstream economists. And he received very little recognition.

In fact, very few even knew about his book for decades.

But that all changed after the 2008 Great Financial Crisis (GFC). . .

Many dusted off Minsky’s work and realized that he effectively wrote the playbook for what would happen between 2001-2009. Hence the Minsky Moment was born.

Minsky wrote about the inherent instability in markets and economies through feedback loops between risk tolerance and credit. But most importantly, how periods of calm are the seeds for future volatility; and vice versa.

He called this the Financial Instability Hypothesis (FIH) – which is now known as the Minsky Moment.

To put it simply, the FIH has two big parts to it:

First – both external and internal shocks drive market crises.

Many economists believe that a bust or crisis only occurs from an external event – for instance, when 9/11 sent prices collapsing. Or when Russia recently invaded Ukraine, sending oil prices surging in Europe.

But Minsky argued that there are also internalevents that lead to a crisis. Such as when perceptions change, which spurs credit booms – and the inevitable busts.

For instance, when investors grow complacent during calm times – they take on more risk and leverage.

But eventually – all this added risk and debt that piles up reaches a tipping point on its own (private debt can’t go up forever).

And suddenly, perceptions change. And the risk-taking behavior rubber-band snaps towards risk aversion and deleveraging.

The crowd rushes to liquidate and salvage what they can. Sending markets and prices sinking. Tightening credit conditions. And thus amplifying the downside lower (think about 1929 or 2008).

And this snap from risk-taking to risk aversion is part one of the Minsky Moment.

Or said another way, the good times are the seeds for future bad times. And vice versa (because eventually the overselling, fear, and deleveraging will end, and the risk-taking behavior comes back).

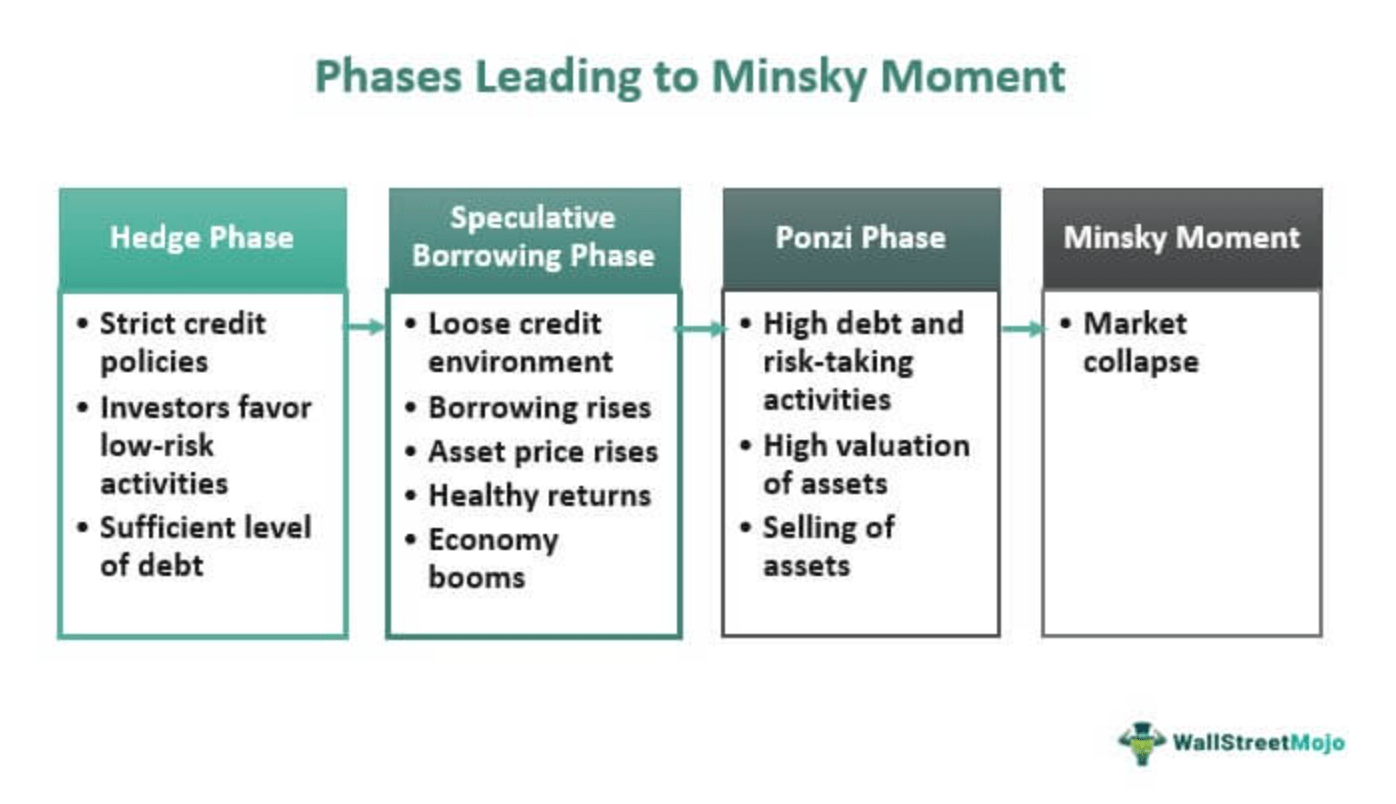

Now, second – there are three stages of financial regimes in the private economy that move towards instability all on their own.

It starts with hedged finance – when consumers or companies make enough cash flow to repay both principal and interest on the debt (the safest regime).

Then there’s speculative finance – when there’s only enough cash flow to repay interest on the debt (the worrisome regime).

And finally, Ponzi finance – where cash flow can’t repay either interest or principal, thus new debt is always needed to repay old debt (unsustainable regime).

As you can see – both parts of the financial instability hypothesis feed off of each other.

Thus according to Minsky, financial crises occur when the economy moves from the hedge finance stage to the speculative or Ponzi finance stages, as increasing levels of debt and risk tolerance lead to a buildup of financial fragility and vulnerability. When a shock or disruption occurs – such as a decline in asset prices or a slowdown in economic growth – borrowers may become unable to meet their obligations, triggering a wave of fear, defaults, and a breakdown in the financial system.

And this tipping point into collapse is the infamous Minsky Moment (I’ve written more about this before – read here).

It’s clear from this perspective – and history – that markets trend toward disequilibrium more often than not.

And that’s what makes Minsky and his financial instability hypothesis so important.

George Soros and his Theory of Reflexivity: How Feedback Loops Drive Markets Too High – and Too Low

George Soros is a Hungarian-born investor that’s best known for ‘breaking the Bank of England’ (the BoE) in 1992.

How did he do that?

In short, he believed that the British currency – the pound sterling – was too strong and strangling the economy. Making matters worse, the pound was effectively pegged to the German currency in the Exchange Rate Mechanism (ERM – which was essentially the first step in what would later become the Euro).

Thus, Soros saw an opportunity to force the BoE to devalue their currency sooner than later.

Or rather, push the BoE to fall on their face instead of limping along.

Soros made huge short bets on the pound, putting pressure on it. And as others saw what he was doing, more shorts piled in. This forced the BoE to cut interest rates and break their peg – devaluing the pound.

Soros made out like a bandit – netting over $1 billion in a single day (remember a billion was worth much more in 1992).

Now – say what you will about Soros (he’s a very divisive character) – but the thesis he used to determine this opportunity was brilliant.

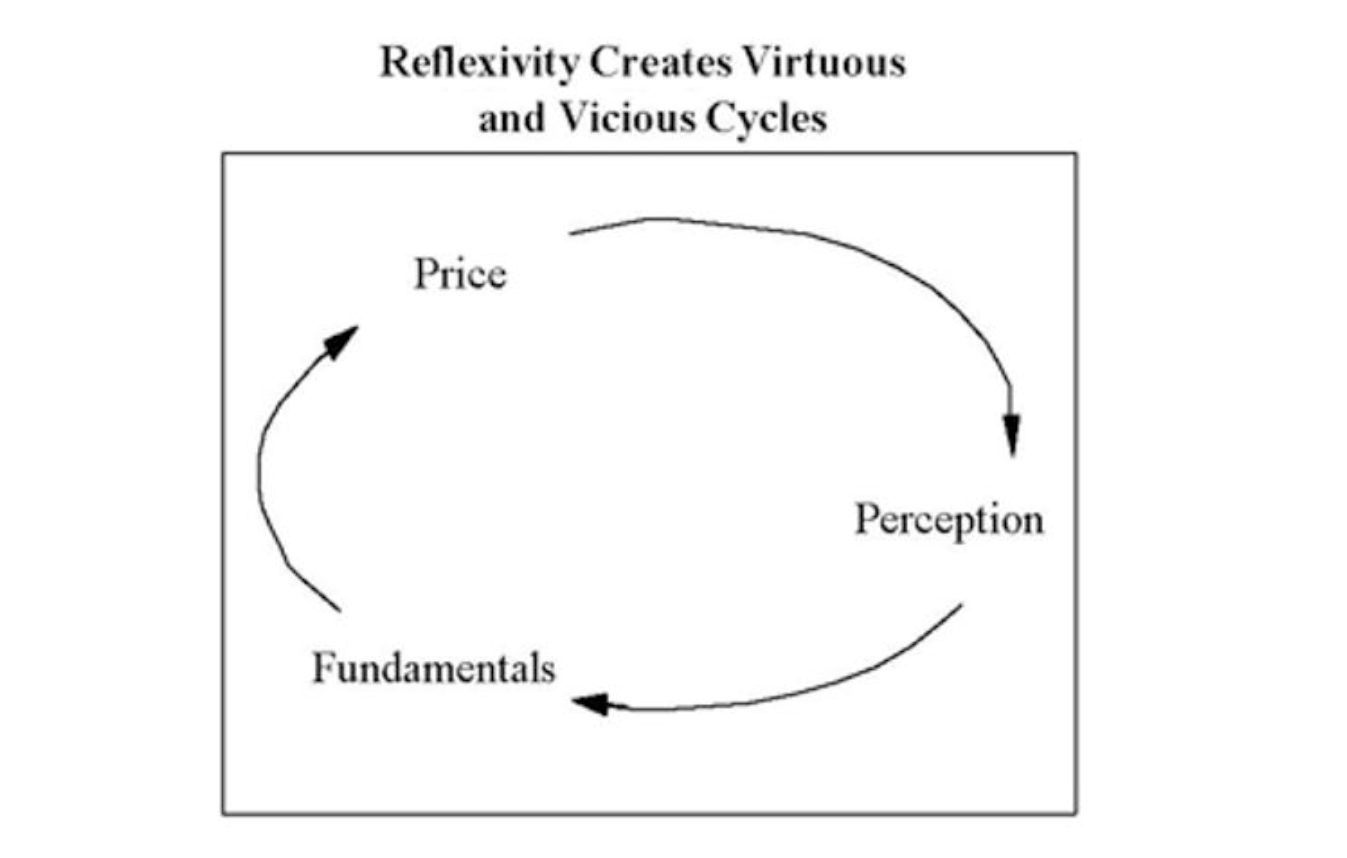

He called this the Theory of Reflexivity.

To put it simply, reflexivity means that crowd expectations, prices, and economic fundamentals feed off each other. Thus creating amplifying feedback loops in the system that spiral too far away – up or down – from equilibrium. And will always eventually reverse.

According to this theory, reality is not an objective and fixed entity. But is instead shaped by our subjective perceptions and interpretations.

In other words, our understanding of reality is not passive, but active, as we contribute to shaping it through our actions (a self-fulfilling prophecy).

And while Soros didn’t invent the term reflexivity (he got the inspiration from philosopher Karl Popper), he applied it in financial markets.

For example, if investor perception is optimisticabout tech stocks, then they buy up shares expecting higher growth. This pushes prices higher and creates further buying as the crowd piles in. Meanwhile, this has reduced the cost of capital for tech firms’ since they can now issue equity at higher prices very easily. And with that money, their balance sheets look better and they can expand capacity, further reinforcing optimism by the crowd and more buying. Thus repeat.

And this works vice versa when investor perception is pessimistic.

It’s not hard to see how sentiment, fundamentals, and prices feed off each other to create a virtuous cycle. Amplifying both booms and busts.

Thus Soros showed that the reflexive process is particularly relevant in financial markets, where investors’ perceptions and actions can have a significant impact on asset prices and market conditions.

He made a point that financial bubbles and crashes aren’t caused solely by external factors – such as economic fundamentals – but also by the reflexive feedback loop between investors’ perceptions and their buying/selling actions.

So in summary, it’s important for speculators to keep these two concepts in mind – the financial instability hypothesis and the theory of reflexivity – when navigating markets.

Gauging sentiment and understanding the causal link it has to fundamentals is critical. As well as the inherent feedback loops that propel markets both irrationally high and low.

So while many cling to equilibrium theories and rational markets, we will know better.

Next time you hear someone preaching about how investors and markets are efficient – keep Minsky and Soros in mind.

**NOTE: both Minsky and Soros’ books are extremely important reads and part of the Speculators Anonymous comprehensive reading list.