The Commercial Real Estate Market Is A Ticking Time Bomb For Small Banks

It’s been almost three weeks since Silicon Valley Bank (SVB) blew up. With both NY Signature Bank (SBNY) and Credit Suisse (CS) following right behind it.

Now, I recently touched on SVB and the chronic issues plaguing U.S. banks.

But there’s one issue that’s really worrying. . .

And that’s the ticking time bomb in the commercial real estate market – which is especially dangerous for smaller banks.

Why?

Because smaller banks – such as local and community banks – are sitting on a pile of toxic commercial real estate loans.

And I expect things are nearing a tipping point. . .

Let me explain.

Commercial Real Estate: Things Are Growing Very, Very Fragile

So, what is commercial real estate?

Putting it simply, commercial real estate (CRE) refers to properties used for business or investment purposes, rather than for personal residential use. Meaning office buildings, retail spaces, industrial properties, warehouses, multi-family (apartments), and other types of commercial properties.

Commercial real estate is typically purchased, leased, or developed with the purpose of generating income through rent or resale. Investors and businesses may also use commercial real estate for their own operations, such as leasing office space for employees or storing inventory in a warehouse, etc.

In other words, commercial real estate is essentially used for work-related business and thus drives income from such activities.

And this is a huge market.

For instance, the commercial real estate market is worth around $20 trillion.

And after decades of surging growth fueled by low-interest rates and easy credit, commercial real estate is now hitting a brick wall.

And I believe there are three main reasons for this commercial real estate stress:

I. Higher interest rates – which tend to decrease marginal demand for expansion by businesses (less space required), eat into landlord earnings, weigh down asset prices, and also increase the cost of debt.

This is a big problem for commercial real estate as it’s a highly leveraged sector (aka debt-dependent).

It’s estimated – according to the Kobeissi Letter – that over the next five years, more than $2.5 trillion in commercial real estate debt will mature.

Keep in mind this is far more than in any other five-year period in history.

Thus rolling over such a massive amount of debt has become much more expensive at a time when prices keep falling. And defaults are already beginning – such as Brookfield Asset Management and PIMCO failing to recently refinance.

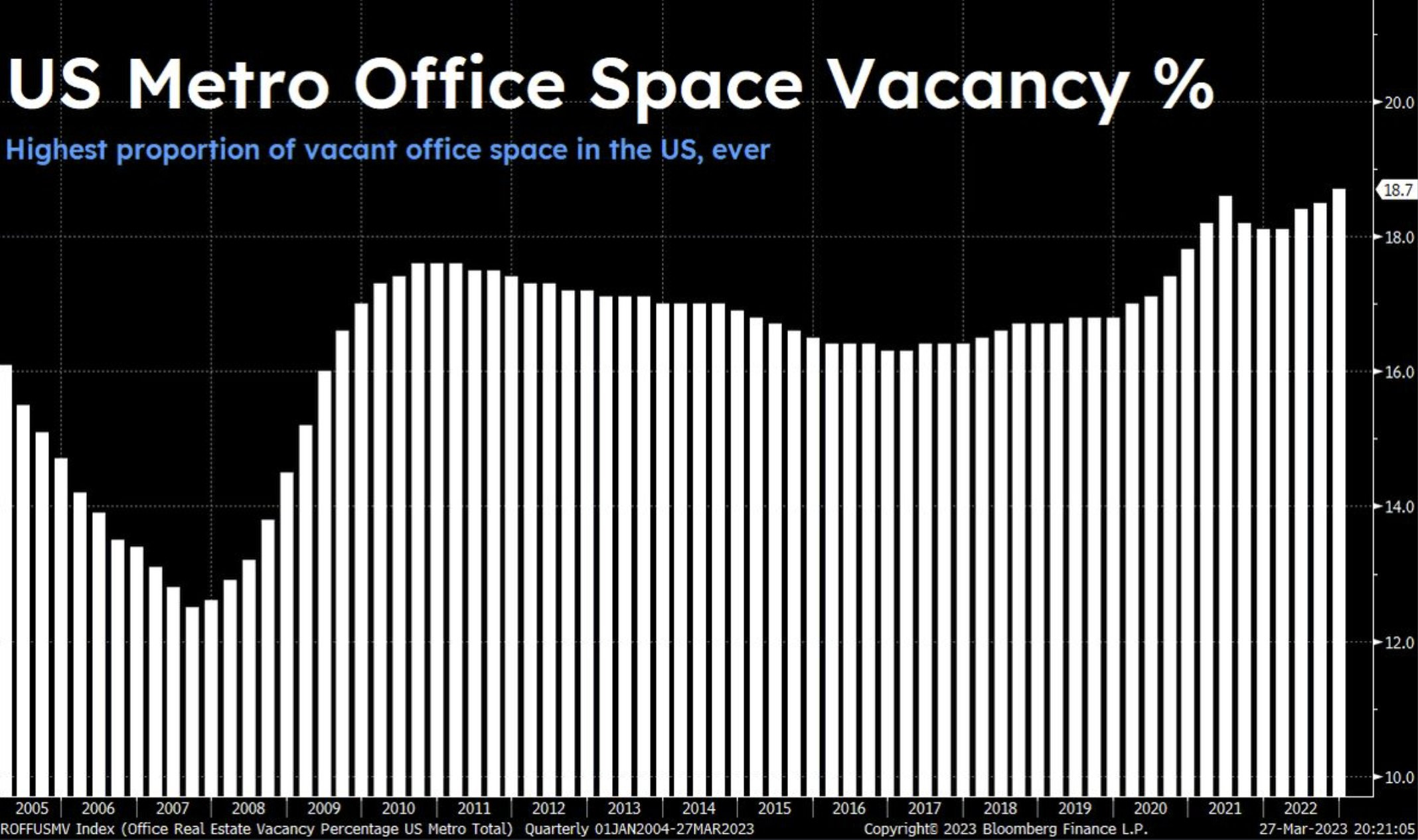

II. Office space vacancies mount as businesses struggle to get workers to come back into the office.

For context, over 25% of U.S. employees still work remotely (up from 5.7% in 2018). And U.S. metro office space vacancies just hit 18.7% – which marks an all-time high.

This matters because if more individuals work from home, companies don’t need excess office space. So they’re canceling leases, or simply selling marginal properties.

And we’ve seen this over the last year as companies – from Meta and Intel to Chevron and Wells Fargo – downsize in big ways.

Breaking leases and selling commercial real estate will further eat away at rent margins and sink property prices (as supply overwhelms demand).

III. There was a glut of commercial real estate built over the last few years. And there’s still a ton coming online.

For perspective – as of February 2023 – there’s about 125 million square feet (M-sqft) of office space under construction. And another 271.3 M-sqft in the planning stages.

Making matters worse – according to CoStart – there’s currently 232 M-sqft of surplus commercial real estate up for subleasing. Which is twice the level from before 2020.

Now, I expect much of that planned construction won’t continue. But what’s already being built is a huge amount.

Thus – as I’ve written about before regarding the capital cycle – these builders are adding supply into a glut (typical in the late stage of the cycle).

This will weigh down building prices and rents further as the supply increases at a time when demand is already anemic.

So, it’s not hard to see that the commercial real estate market is growing increasingly fragile from both structural issues (debt and work-from-home) and cyclical downside (higher interest rates and overbuilding).

But the big question is, who’s most at risk of further downside?

Commercial Real Estate and Smaller Banks – An Unbalanced and Fragile Dance

I think it’s clear that the downside in commercial real estate outweighs any upside in the years ahead.

And while many focus on this aspect, I’d rather look at what negative ripple effects this will cause.

Hence why I’m looking at smaller banks. . .

Now, what do I mean by smaller banks?

The U.S. government describes small banks (or rather community banks) as having assets of less than $1.384 billion in either of the last two calendar years.

So – according to recent data – that’s about 3,725 banks in the U.S. (out of the roughly 4,200 total commercial banks)

And while these ‘community’ banks hold less than about 10% of total assets in the banking system (give or take) – they’re the lifeblood in smaller and rural markets.

So, what’s the issue here?

Well, these community banks are extremely exposed to the commercial real estate market.

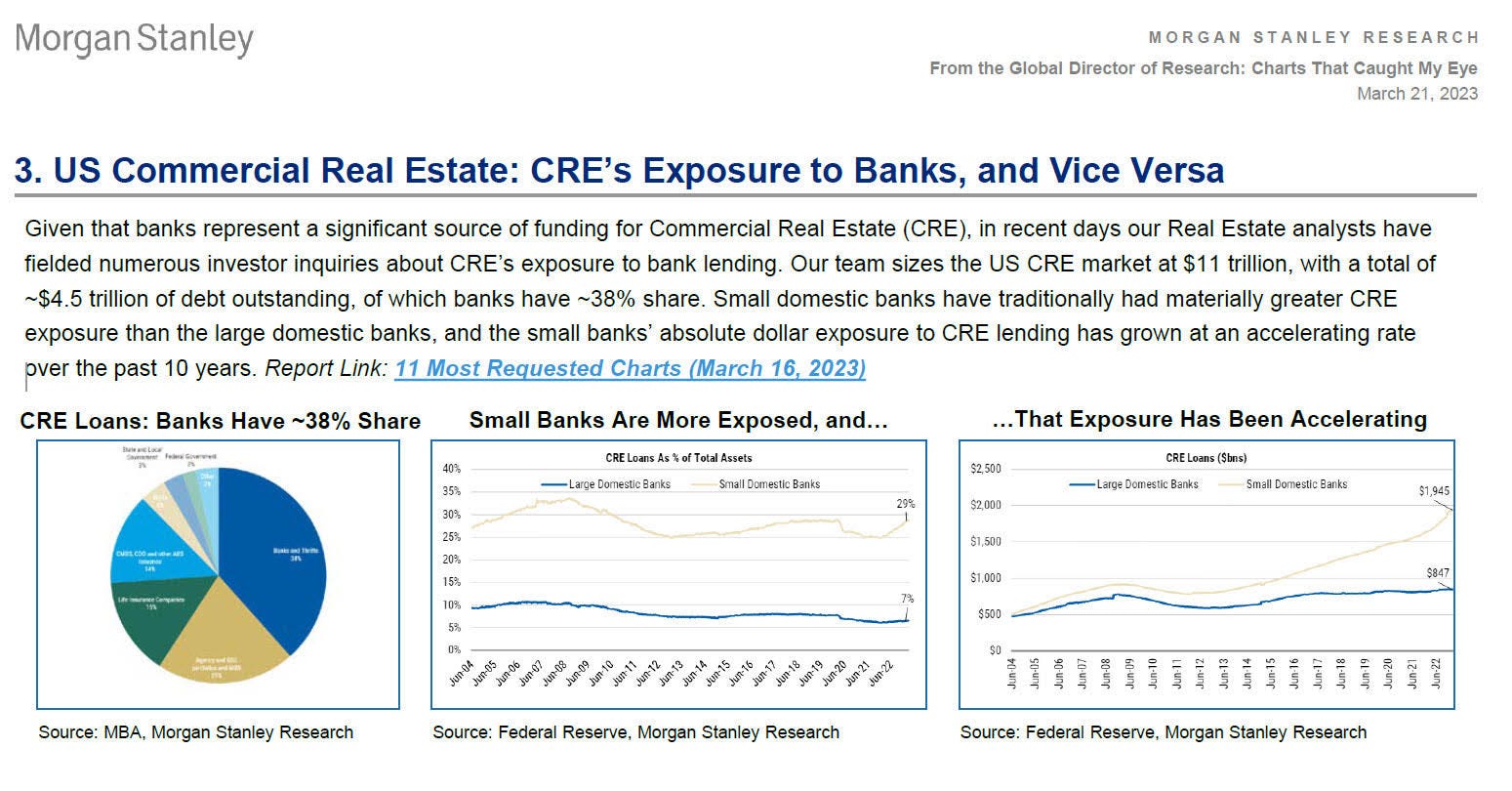

To put this into context – according to Morgan Stanley – U.S. banks currently hold roughly 38% of all commercial real estate debt.

Meaning banks hold $1.8 trillion of the total $4.5 trillion debt.

And out of that, nearly 30% is held by small banks (compared to just 7% for large banks).

More worrisome is that the acceleration in commercial real estate loans by small banks has soared over the last decade. Rising from roughly $800 billion in 2012 to $2 trillion in mid-2022.

But most troubling is the sharp rise in the last two years. . .

And according to MSCI Real Assets, landlords received about 27% of financing from local and regional banks in 2022 – which was the biggest source of newly originated debt.

Other data – according to Goldman Sachs via FT – shows banks with less than $250 billion in assets make up about 80% of commercial real estate loans.

Thus it’s no stretch to say that the smaller banks are disproportionately leveraged in the commercial real estate market.

But here’s where the amplifying feedback loop comes in. . .

Since commercial real estate depends on a hefty amount of financing from smaller banks, these smaller banks also depend on commercial real estate prices and incomes.

When income streams from leases and property values rise, banks will make loans (as it’s profitable and secured by increasing property prices).

But when property prices (which back the loan) fall, and incomes erode (increasing default risk) – things sour.

Banks won’t extend new loans into the sector. And without new financing, these commercial real estate owners can’t roll over their debt. So they’ll sell, pushing down prices further as supply increases relative to anemic demand.

Thus reinforcing the feedback loop as banks suffer losses and tighten credit further. And on and on.

So, why does this matter now?

Because since early-2022, banks have started tightening credit standards in big ways. Especially in the commercial real estate market.

For instance – over the last year – the net percentage of domestic banks tightening credit standards for commercial real estate loans has soared to 70% in Q1-2023.

This is problematic as a tidal wave of commercial real estate debt comes due in the next few years – with $900 billion maturing by 2025.

And these owners need access to credit.

Without it, they’ll end up forced to default and liquidate.

This will also affect smaller bank balance sheets in a big way. Since they’re extremely entrenched in the commercial real estate sector.

For instance – after SVB collapsed in early March – it put a bright light on the massive losses facing loan books for commercial real estate debt.

When regulators sold off $72 billion from SVB, it went for a $16.4 billion discount from what they were “valued” at on their books.

That means they went for roughly 77 cents on the dollar (or a 23% discount).

Now, it’s important to say that not all of the assets sold off from SVB were commercial real estate related. Roughly just $3 billion of their $13 billion real estate loans were commercial real estate.

But this gives us a look at the potential issue banks are facing with unrealized losses (meaning the prices they’ll get if sold on the market).

Or – putting it another way – smaller banks are going to have to deal with some serious write-downs (i.e. the difference between what they think their worth vs. what the market will pay)

For perspective, Barclays expects office-building valuations to drop by 30% over the next few years.

This will put steep pressure on small-to-medium bank loan books – since they’ve extended most of the credit to this sector.

Making matters worse, small banks have seen deposits fly out the door after the SVB blowup.

Smaller banks saw deposits drop by a record amount – down $109 billion through March 15th. And over $200 billion by the 27th.

This marks a 1.5% year-over-year decline – which is the first annual drop since 1986.

And if these smaller banks suffer further deposit outflows, they may have to sell assets in a hurry (and at a discount).

It’s important to remember that banks are black boxes – aka something with internals that are usually hidden or mysterious to onlookers.

Even the best analysts don’t really know what bank loan books are truly worth.

But one thing seems clear, the commercial real estate sector is growing more and more fragile.

And with it, so are the smaller banks that extended credit to them.

The black swans are lurking.