Anatomy of a Blowup: SVB is The First Domino To Fall – And More Are Coming

Markets continue to roil from the second and third largest U.S. bank busts in history – Silicon Valley Bank (SVB) and NY Signature Bank (SBNY).

SVB was the 16th largest bank in the U.S. – SBNY was roughly the 36th (although it’s not a technical bank).

Both effectively failed within days of each other.

Or putting it another way – a bank run occurred at SVB (when customers lose faith in an institution’s ability to look after their money and pull their money out). And it spread to SBNY.

Now, Credit Suisse (CS) – the second-largest bank in Switzerland and a major player in international finance – is imploding. Potentially leading to a euro-banking crisis. And First Republic Bank (FRC) – the 22nd largest bank in the U.S. – is teetering at the edge of insolvency.

In the meantime – government policies are trying to band-aid things over.

But clearly, the cracks are spreading.

Will it last? Who knows.

But I believe there are deep structural imbalances building in the financial system. And that things continue to grow more fragile – especially with each Federal Reserve rate hike making it worse.

Here’s what you need to know. . .

Brief History: How The Treasury and the Fed Caused a Glut of Deposits During COVID-19

Many probably have read about SVB and SBNY already.

And many pundits are solely focusing on the end results.

But I prefer to look at the causal chain (the cause that led to the effect) of events.

So – how did we get here?

Well, long story short – after COVID-19 struck in 2020 – the U.S. Treasury and Federal Reserve ran massive stimulus programs.

For context, the Fed injected some $4.7 trillion through asset purchases (like Treasury bonds and Mortgage-Backed Securities from banks, giving them deposits instead). And the U.S. Treasury injected some $5.6 trillion into the economy – things like PPP loans, direct checks, tax credits, and state funding.

This sent the U.S. debt-to-GDP from 107% in early-2020 to 121% as of winter-2022. And the Fed’s balance sheet roughly doubled from $4.1 trillion to $8.5 trillion in the same period.

This is an ungodly amount of liquidity pumped into the system in such a short span of time.

And while many saw the headlines focusing on the stimulus saving the economy, it’s the ‘unseen’ that matters. . .

And that was the enormous flow of deposits hitting banks – increasing fragility.

In the last three years, banks saw massiveincreases in their deposits.

And that’s because of all the stimuli – like PPP loans, and direct checks to consumers – which went into bank accounts. Thus inflating bank deposits.

Why does this matter?

Because banks were drowning in deposits and not making enough loans – a dangerous combination.

Remember that deposits are a liability (banks owe interest on deposits). It’s not their money. So a tidal wave of deposits isn’t healthy for a bank if it just sits there eating away at their margins.

That’s why banks make loans – it’s an asset for them. They collect the interest on loans and pay the depositors their interest. And profit from the difference.

As the old saying goes, “banks borrower short and lend long.”

So when banks saw these tremendous inflows, they scrambled to put it to work.

But they’ve struggled to do so.

For instance, U.S. bank loans-to-deposits – the ratio of bank liquidity – have declined sharply since 2019. (Albeit it’s recovered in 2022 as consumers borrowed at record amounts and deposits declined, flowing into things like money market funds and other vehicles).

Adding even greater uncertainty is that banks are beginning to tighten lending standards dramaticallyover the last three quarters straight (I’ve written more about this recently – read here).

And this will most likely cause loan growth to slow (making the loan-to-deposit ratio worse).

So putting it simply, banks saw deposits explode at a time when lending was looking anemic.

(Keep in mind I’m over-simplifying things but that’s the gist).

Now, that brings us to SVB and SBNY. . .

SVB and SBNY – Rapid Growth in Concentrated Sectors Was Very Fragile

Now that we got the mere basics out of the way, how did this glut of deposits help lead to both SVB and SBNY’s collapse?

Well – for starters – SVB and SBNY saw a massive amount of deposit growth from all the post-2020 stimulus.

According to Wells Fargo – SVB’s total deposit growth soared 420% since 2017. And SBNYs grew 270%.

To put this into perspective, total U.S. commercial bank deposits only grew 153% in the same period.

These banks roughly doubled and tripled in sizewithin two years (2020-2022).

And as I mentioned above, a bank can’t just sit on deposits. They need to create loans (assets). Otherwise, they’ll bleed money paying interest.

Now, most of SVB’s deposits were uninsured and extremely concentrated in the tech sector and venture capital (VC) sectors.

So as account balances among many of the start-ups began declining over the last year amid less VC funding – deposits began suddenly dropping.

For instance, when a bank or VC issues a loan or investment to an unprofitable tech startup (which most are), it creates a deposit. And since most of these firms banked with SVB, it became theirdeposit.

Thus with fewer loans and funding, firms were burning through their cash without re-adding to it. Causing deposits to decline.

Journalist and macro researcher – Jack Farley – showed this exact point.

So amid declining lending to start-ups that banked with SVB and eroding deposits, all it needed was a couple of big players (like Peter Thiel’s Founders Fund) to pull their money out and trigger a bank run.

This made SVB extremely fragile.

Meanwhile, SBNY had risen as a major leading lender and investor in the cryptocurrency market post-2020. And after SVB fell, a ‘crisis of confidence’ spread to them. Causing SBNY to lose ~20% of deposits within a single day. Rendering them insolvent.

Now after focusing on their liabilities – let’s talk assets.

For starters, most often when deposits soar, banks will buy highly liquid and ‘safe’ assets – like U.S. Treasury bills (under two-year maturities).

But SVB went for that extra yield. And was buying longer-dated assets – such as mortgage-backed securities (MBSs) and bonds – at the very top of the market (2020-21).

Keep in mind that MBSs have unique features. They get pre-paid when interest rates fall and households refinance. But no one (at least most) refinances when rates are rising.

Thus as rates were rising, SVB’s mortgage bonds were becoming an issue.

Now - thanks to hold-to-maturity (HTM) rules – as long as banks held these assets until maturity, they don’t have to realize losses from lower market values.

Meaning they don’t have to register any losses on their own balance sheets even if the asset prices (bonds here) declined. Because the market value is based on expected cash flows from the bonds.

But this unwinds when a bank's forced to sell these assets on the market or write down the losses from mark-to-market accounting. Then suddenly those losses are real.

So if a bank has a lot of unrealized losses from declining bond values, investors would never even know because the balance sheet wouldn't show them.

And this is why banks are 'black boxes' (aka any complex system with contents that are mysterious). Because even the best analysts can't fully understand what their assets really are.

Thus as deposit outflows overwhelmed SVB, they needed to raise cash. So they sold their assets at steep losses. Suddenly making those losses public.

Sure, SVB could’ve raised interest rates much higher on deposits to attract capital instead. But they would’ve been bleeding income and showing other banks they’re struggling with outflows.

And like they say, the rest is history.

The SVB domino fell, which knocked over SBNY. Then First Republic Bank, and now Credit Suisse.

But I expect this may be just the beginning. . .

The Fed’s Tightening Was The Spark That Started The Banking Fire (As Usual)

As I mentioned earlier, I want to focus on the ‘unseen’ rather than what’s ‘seen’.

And while everyone is blaming incompetent bankers, I believe most of the blame starts at the Fed and Treasury.

We saw bank deposits explode after the post-2020 fiscal and monetary easing. So there’s a clear causal link between the stimulus and massive bank deposits.

And as these banks were forced to absorb these deposits, they scrambled to buy assets at record-high levels.

Then – after pumping all that liquidity into banks – the Fed began tightening in early-2022.

This pushed rates higher – meaning bond prices dropped. It also meant slowing growth – which caused loan creation to sink (since the yield curve inverted to multi-decade levels).

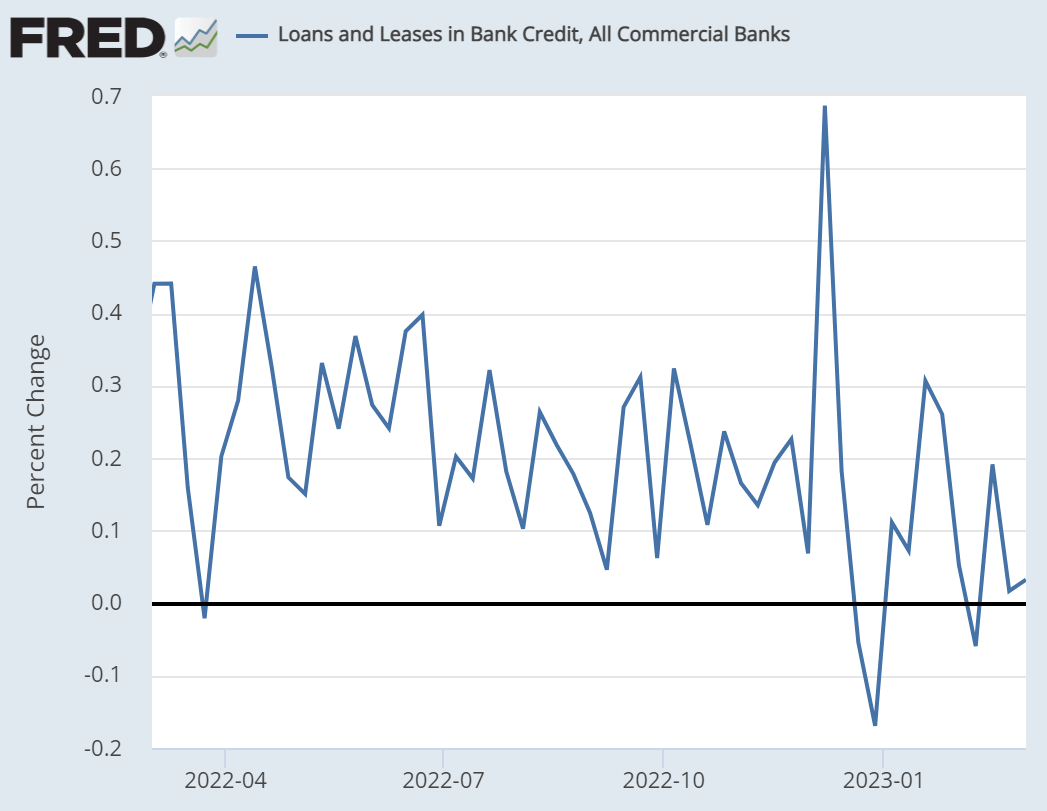

To put this into perspective – take a look at commercial bank loan-and-lease growth (aka credit extended).

It’s declined steadily over the last year.

This puts banks in a distressing position.

The assets they’re holding are falling. Meanwhile generating new loans is more difficult. And the economy is slowing.

So – in summary – I expect further contagion risk in the global banking system. Especially now that some banks have already failed.

Or otherwise said, the cat is out of the hat.

Remember that banks are essentially black boxes – we really don’t know what their exact assets and liabilities are.

Meanwhile, each subsequent rate hike pushes the system closer to a tipping point.

After flooding the system with liquidity, sucking it out through tightening will always come at steep costs.

As the underrated Austrian economist – Ludwig Von Mises – once said, “there is no means of avoiding the final collapse of a boom brought about by credit expansion.”

The black swans are lurking.

*Note: I continue to remain in U.S. long bonds (as I have since October). Because as I shared, the Fed’s tightening deeply inverted the yield curve and would have negative ripple effects throughout the economic and financial systems.